As we

approach the threshold of history's most substantial generational wealth

transfer, we foresee profound changes in asset allocation and valuation. This

pivotal shift—crucial for both families and the economy—signals an era filled

with opportunities and challenges, particularly for Gen X and Millennials. It

is essential to focus not solely on the wealth we inherit but also on our

strategies for the future.

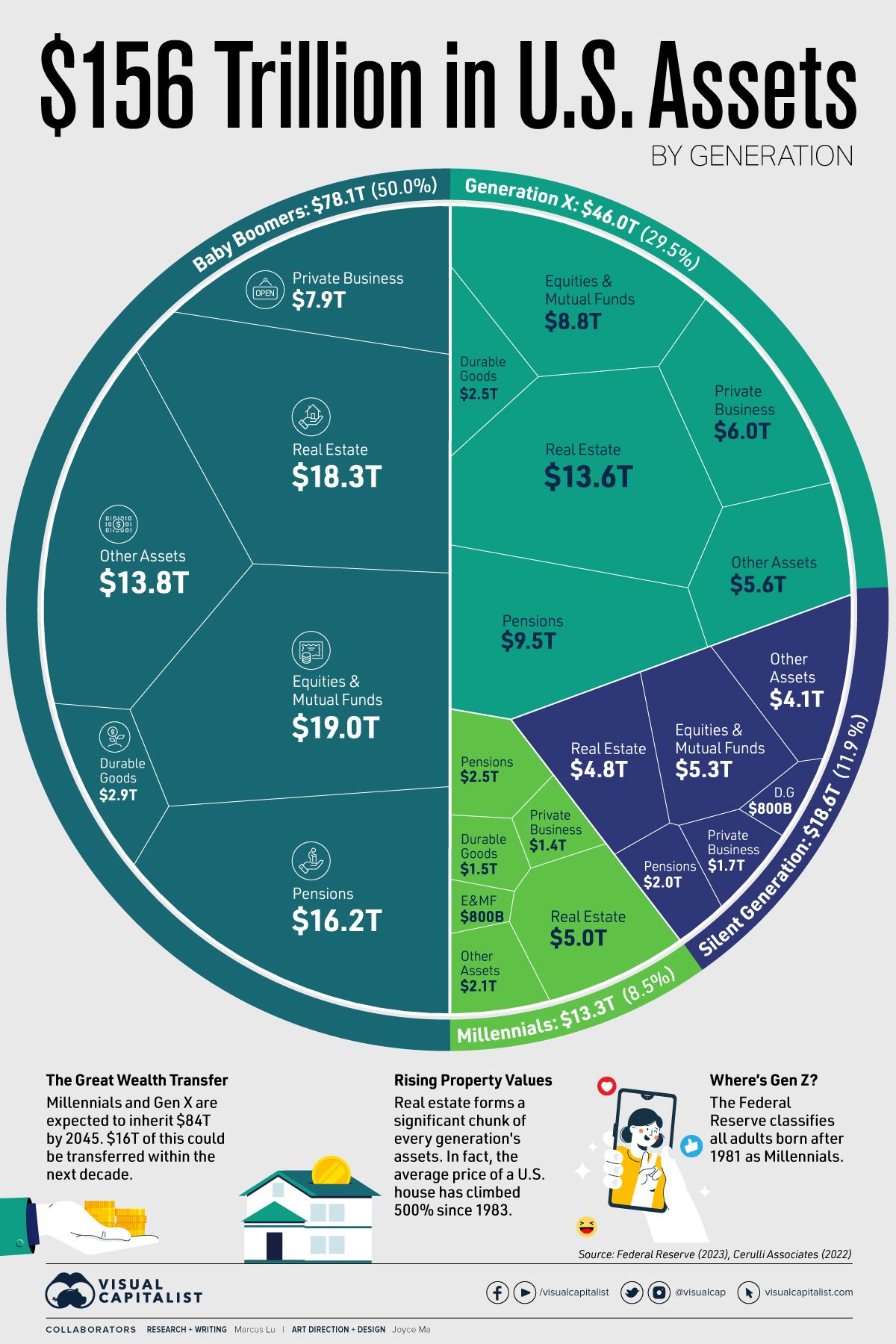

Dissecting Wealth Distribution: A Visual Examination

An analysis of the U.S. wealth pie chart reveals diverse financial landscapes:

Silent Generation: With their wealth concentrated in equities, mutual funds, and real estate, this generation faces the immediate concerns of healthcare and retirement living expenses.

Baby Boomers: Possessing a varied portfolio, Boomers are transitioning toward retirement with a strategic focus on estate planning and long-term care.

Generation X: At the crossroads of home ownership and business investment, Gen X targets wealth accumulation as they enter their prime earning years.

Millennials: Primarily invested in real estate, millennials are beginning to face the realities of wealth building in a fluctuating economy.

Gen Z: Considered part of the Millennial cohort by the Federal Reserve, Gen Z's financial trajectory is yet to be fully defined.

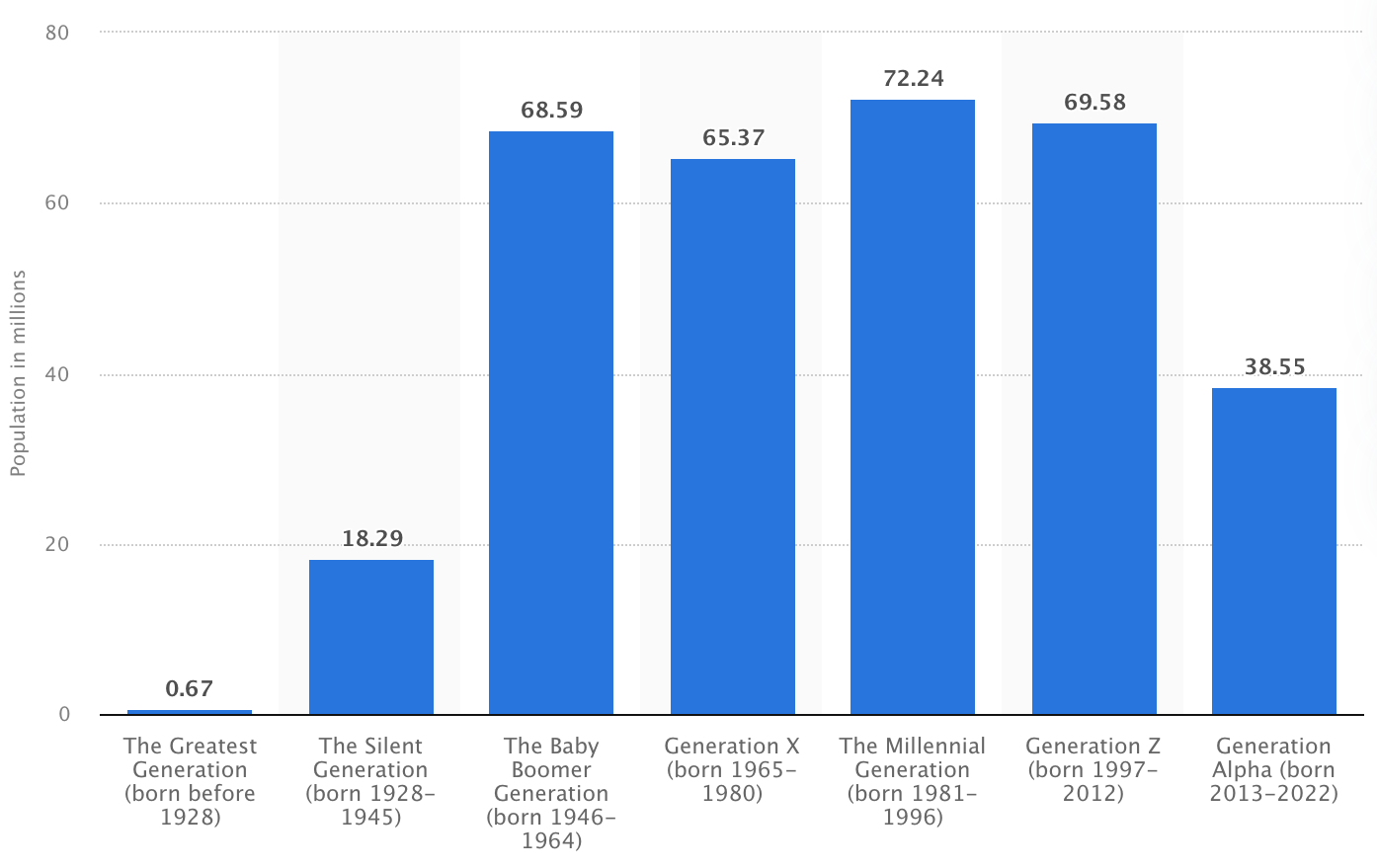

Population Dynamics: A Generational Snapshot (2022)

The Greatest Generation: Born

before 1928

Population: 0.67 million (0.20% of

the total population)

The Silent Generation: Born

1928-1945

Population: 18.29 million (5.49%

of the total population)

Total Wealth: $33.3 trillion

Wealth per Capita: Approximately

$836,523

The Baby Boomer Generation:

Born 1946-1964

Population: 68.59 million (20.58%

of the total population)

Total Wealth: $78.1 trillion

Wealth per Capita: Approximately

$1,138,650

Generation X: Born

1965-1980

Population: 65.37 million (19.61%

of the total population)

Total Wealth: $46.0 trillion

Wealth per Capita: Approximately

$633,318

The Millennial Generation

(excluding Adult Gen Z): Born 1981-1996

Population: 72.24 million (21.67%

of the total population)

Total Wealth: $13.3 trillion

Wealth per Capita: Approximately

$184,109

Generation Z: Born

1997-2012

Population: 69.58 million (20.88%

of the total population)

Generation Alpha: Born

2013-2022

Population: 38.55 million (11.57%

of the total population)

Preparing for the Great Wealth Transfer

The 'Great Wealth Transfer' suggests an impending economic shift, yet for

Gen X and Millennials, the narrative isn't straightforward:

"More than half of Millennials expect to receive an inheritance from their parents or other family members of about $350,000, according to a recent survey by Alliant Credit Union. However, 55% of Baby Boomers plan to leave behind an inheritance of less than $250,000." - Forbes

Expectations vs. Reality: Many

Millennials expect significant inheritances, but these may be thwarted by their

parents' rising healthcare costs, with a potential shortfall of at least

$100,000.

Self-Reliance: The key

takeaway? Don't bank on an inheritance; plan your retirement with prudence.

Ease of Transfers (Liquidity)

Equities & Mutual Funds: Most liquid; can typically

be sold quickly on the stock market

Pensions: Not traditionally liquid; represent cash that can be received on a regular basis once the benefits

begin

Private Business: Less liquid than stocks or

pensions; the time to sell a business can vary

Real Estate: Illiquid; sales typically

taking longer due to the complexity of transactions

Durable Goods: Illiquid; selling goods such

as cars, appliances, or furniture often doesn't recoup significant value and may take time

Other Assets: Liquidity depends on type

of asset; may include both liquid and illiquid assets, generally requires more time to convert into cash compared to equities or

pensions

Entrepreneurship Through Acquisition

Acquiring Established Businesses: The

Baby Boomer generation is approaching retirement in large numbers, creating an

opportunity to purchase established businesses. Look for organizations that

connect retiring business owners with potential buyers, such as SCORE or the National

Federation of Independent Business (NFIB).

Franchise Opportunities: Franchise

ownership provides a proven business model and brand recognition, which can be

advantageous for new entrepreneurs. Investigate franchise opportunities with a

lower initial investment or those focused on specific demographics/sectors.

The Impact of Long-Term Care Costs

Assisted

Living: Averages are $4,807 per month.

Memory Care:

Averages are $5,995 per month.

Independent

Living: Approximately $3,000 per month.

In-Home Care:

Around $30 per hour, with full-time care equating to about $5,720 a month based

on national median rates.

For many adults, the annual retirement health care costs remain uncertain, but planning for these expenses is essential to protect retirement savings.

The Generational Approach to Long-Term Care Insurance

Younger

Generations: Encouraged to

consider long-term care insurance early to benefit from lower premiums.

Older

Generations: Should review

their retirement plans to include potential healthcare needs, exploring

options like life insurance or annuities with long-term care riders.

Estate Planning: An Imperative Step for Everyone, Not Just the Wealthy

Wills

and Trusts: Essential

tools to manage your assets posthumously.

Medical

Directives: Ensuring your

healthcare wishes are honored.

Early

Planning: The earlier

you start, the more you can secure your legacy.

The Realities of Retirement

The

Savings Gap: With rising

living costs, saving for retirement is more critical than ever.

Healthcare

Costs: Long-term care

could erode what you've worked hard to build.

Facing the Future Together: Industry Growth from New Generational Trends

Tech

and Green Energy: Fields that

may offer opportunities for growth.

Healthcare: An ever-important sector given the aging

population.

Review Your Plans: The Power Lies in Preparation

Estate

Planning: It's time to

review or establish your estate plan.

Long-Term

Care Considerations: Assess your

potential medical expenses in advanced age.

By embracing proactive planning, and with the help of a financial advisor you trust, you can navigate the complex terrain of generational wealth with confidence and clarity.