How to Manage Your Debt No Matter What Size It Is

When you need additional funds to cover your urgent expenses, you

often opt for different lending options such as personal loans or credit cards.

If you have some debt you need to manage it.

Making regular payments will help you prevent the debt from

getting out of your control. When you have a lot of debt, it can be more

challenging. Here is how proper debt management can help you manage your

payments and get out of debt.

Pay Your Monthly Bills

Having a debt management plan is essential if you want to have

your funds in order and pay the debt off on time. Late monthly payments may

make it more difficult to become financially free. Late payments are often

associated with late fees and penalties. Nobody wants to pay additional charges

and increase the total cost of borrowing.

If you take out a Fit My loan and know how to manage debt you will most likely

make on-time payments whether they are weekly or monthly. Otherwise, finance

charges and interest rates will increase.

Know the Exact Sum You Owe

The first thing you should do is be aware of the

real numbers you owe. Do you know all the debt you have? Crafting a list can

help you see the whole picture. Write down the lender or crediting company, the

sum you owe, the interest rate, the monthly payment as well as the due

date.

Do you have doubts if you forgot something? Get

your free annual credit report to check this information. The three major

crediting agencies can give you a copy of your report to confirm what debt is

on your list.

Calculate Your Debt to Income Ratio

You can calculate your DTI once you know how much you owe and how

much you earn each month. Are you sure how much of your income is used for debt

payments? If not, a debt-to-income ratio will show you. You need to divide your

debt payments by your income and multiply by 100.

For instance, if you have $1,200 of debt and your monthly income

is $3,000, you will get 0.4 x 100 = 40%. It's always good to have this figure

lower. So, if you keep on tracking your DTI you will have a better

understanding of your personal finances.

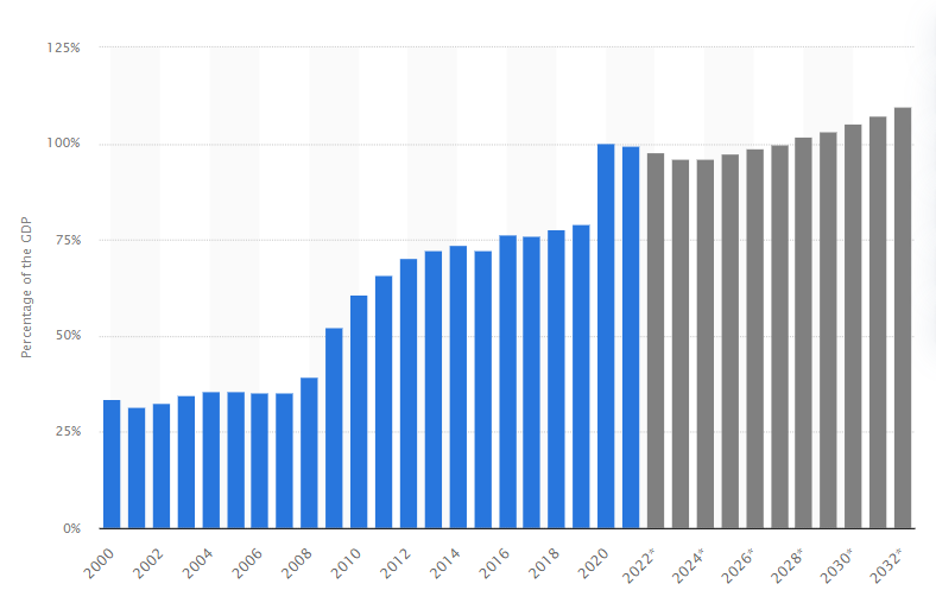

Debt Statistics

Many people accumulate debt.

This is a common issue for millions of individuals. According to Statista.com and its report on personal debt in the U.S.,

public debt has grown steadily since 2008 and continues to rise. The 2021

survey shows that two in three Americans are in debt.

People find different sources

of debt. Credit card and mortgage debt accounted for 43 percent of all consumer

debt last year. While mortgage rates are typically low, credit cards can be

quite expensive in terms of interest rates.

High rates may make it harder

to repay credit card debt. Economists and financial experts state that personal

debt has the power to fuel economic expansion. Cheaper crediting options are

available to consumers today while increased demand for consumer goods can help

to boost economic growth and domestic production.

Have a Budget

Would you like to learn how to manage credit card

debt? Create a monthly budget and stick to it. This system can help consumers

avoid debt or get out of it faster. Having a budget means you know where your

money goes.

You should try your best to spend your monthly

income only on necessities and financial obligations. All money that is left

after you pay the regular bills, rent, and groceries should go toward debt

repayment.

Make At Least the Minimum Payments

It takes time and effort to manage debt and reach

financial independence. Some experts may advise you to allocate more money for

debt repayment. However, not every borrower can afford to pay more. It all

depends on your monthly paycheck, regular employment, and spending

habits.

If you are dedicated to getting rid of debt as

soon as possible, it pays to make more than the minimum monthly payments on

each debt you have. If you can't afford it, make at least the minimum payments.

You will also notice the positive changes, while your account will remain in

good standing and you will avoid late penalties.

Choose The Type of Debt to Repay First

You may have several types of debt such as a

mortgage, a credit card, a student loan, a personal loan, etc. Each of these

forms of debt comes with certain rates and repayment terms. Most borrowers

can't have all their debts under control at the same time. Tackle one debt at a

time.

You may want to start repaying the debt with the

highest interest to save your money. It should be your top priority to cover

the necessary payments until the highest interest debt is paid in full. Rank

and prioritize your debts until the smallest one is left.

Create an Emergency Fund

The last tip is to make an emergency fund to

protect you from the upcoming disruptions with personal funds. If you don't

have access to your savings, it's much easier to get into trouble.

Small savings of a portion of your paycheck so

that you set aside some cash. Don't utilize it for purchases or entertainment.

It should be your fund for the rainy day that will help you avoid more debt by

funding any emergency with your own savings.

In conclusion, debt of any size can be managed

and repaid. It takes some effort and time to build healthy spending habits and

improve your financial literacy to avoid mistakes. If you feel overwhelmed with

the amount of debt you have, you may want to turn to a credit counseling agency

for professional guidance. Debt settlement or debt consolidation may be helpful

for your debt relief.

{kind=link}